Great strategy (banks)! Chasing yield (hedging against USD) when a 'shit storm' of risk averse news hits the wires in next 48hrs

The hedge funds will be in the money though (triple top).

So where is the capitulation point? Obviously 0.87

Thursday, July 29, 2010

Dow showing selling pressure after two days of range trading

A very tight range trade of two days from the 26th July 2010 to the 27th July 2010 after breaking out of it's volatility spread on the 22nd July 2010. This break out from 10300 was mainly to do with q2 earnings. The Dow is now topped at 10541 with a sell pressure on, note all volume indicators to volume show divergences, indicating that liquidity is not pouring into the Dow and stocks. Also evident of bigger funds/investment banks chasing higher yields for the end of July 2010 consolidation. This can be seen with USD weakness and high yield currencies buys (potentially a bad bet but nevertheless a short term mega buy, especially if China's PMI release in early August 2010 is weak, US GDP figures are weak, and Japanese retail investors cutting long position on carry trade currencies; a major sell on high risk/yield assets will ensure).

The Dow should fall back into it's volatile based trading ranges, with further selling pressure in the next 5 mths the 10000 breach should not be ruled out as all major indices have topped out for the half year major selling activity will continue; especially when yields remain weak on the 10yr and 2yr Treasury's and should fall lower effecting stock gains.

H2 could see risk aversion remain as the sell factor.

Green (26th July 2010) and Red (27th July 2010) horizontal lines

Note massive divergence between Volume and OBV and ACD (horizontal dotted line)

The Dow should fall back into it's volatile based trading ranges, with further selling pressure in the next 5 mths the 10000 breach should not be ruled out as all major indices have topped out for the half year major selling activity will continue; especially when yields remain weak on the 10yr and 2yr Treasury's and should fall lower effecting stock gains.

H2 could see risk aversion remain as the sell factor.

Green (26th July 2010) and Red (27th July 2010) horizontal lines

Note massive divergence between Volume and OBV and ACD (horizontal dotted line)

{kind=link}

Wednesday, July 28, 2010

Japanese FX margin traders (retail/Mrs Wantabes) about to get a leverage shakeout.

The Japanese Financial Service authority is just about to change the rules of the 0.50% leverage to 0.25% and most Japanese retail investors are holders of long position/s on the AUD and NZD and YEN crosses (with leverage at 1:100)

Some major selling going to take place: August 2010

" The yen may climb next month as tighter regulations force Japanese households controlling about $76 billion in daily exchange trading to unwind bets on higher- yielding currencies, analysts said.

The government will cap debt used to boost trading bets, or leverage, at 50 times committed cash from August 2010, down to 25 times in 2011, the Financial Services Agency decided last year. Individual traders have started to prepare for the change, according to Japan’s biggest online currency broker which saw accounts with 100 times or more leverage fall by half last month."

"Trinh recommends selling the Australian dollar, saying it may retest the 72 yen level reached in May amid ebbing sales in Japan of overseas-focused mutual funds and a pattern of seasonal weakness for the Aussie in August.

Net short positions on the yen, equivalent to yen carry trades, stood at 1.89 trillion yen ($21.6 billion) at the end of June, up 59 percent from the previous month, according to the Financial Futures Association of Japan, which compiles data from 57 margin brokerages."

0% interest rates (US), money printing: but where is all the money going?

The US and the global banking system was close to implosion in 2008, with balance sheet holes that were so billion dollar big it was unprecedented. The US government's $700 billion dollar (TARP) bailout monies was gobbled up in large portions from Wall Street and America's biggest banks like Citigroup and Bank of America. After more than two years the banks are still reliant on tax payer assistance as the banks and credit lenders appear to be sucking more money in than money going out i.e profits. As discussed in The 2009 'Obama bounce' / liquidity rallies have come to an end. (*revised) we are seeing profits down but revenue up, which translates to a money supply orientated boost in revenue, but unable to maintain profit even with constant or growing revenue. This occurred recently with Visa, "Visa Inc.'s (V) fiscal third-quarter profit dropped 1.8% from a year ago but revenue jumped 23% as consumers ratcheted up spending and the company processed more payments."

So with profits falling and revenue looking stretched (refer to Citigroup lower profit at 37% and low revenue, which means that the bank has cut it's risk position in the market) and a drying up of the M3 money supply refer to chart:

A funding/liquidity squeeze mixed with a possible new credit crunch (via banks utilizing risk again) could lead to a festering banking problem in the US.

US banks are still going bust with 7 banks failing on the 27th July 2010, it would appear that the banking crisis and credit crisis is still lurking that could strike the bigger banks at some point (further write-downs). With Basel 111 rules being somewhat delayed till 2018, if the banking sector decides to take on risk again to boost profits ala from the CMBS market, or other derivative markets. A new credit crunch will ensure.

Despite 0% rates and a peak in money supply in 2008/2009 liquidity has either drained out quickly (via Fed refinance operations), and/or has been sucked into depreciating 'black holes' on US bank balance sheets.

So with profits falling and revenue looking stretched (refer to Citigroup lower profit at 37% and low revenue, which means that the bank has cut it's risk position in the market) and a drying up of the M3 money supply refer to chart:

A funding/liquidity squeeze mixed with a possible new credit crunch (via banks utilizing risk again) could lead to a festering banking problem in the US.

US banks are still going bust with 7 banks failing on the 27th July 2010, it would appear that the banking crisis and credit crisis is still lurking that could strike the bigger banks at some point (further write-downs). With Basel 111 rules being somewhat delayed till 2018, if the banking sector decides to take on risk again to boost profits ala from the CMBS market, or other derivative markets. A new credit crunch will ensure.

Despite 0% rates and a peak in money supply in 2008/2009 liquidity has either drained out quickly (via Fed refinance operations), and/or has been sucked into depreciating 'black holes' on US bank balance sheets.

Tuesday, July 27, 2010

Brutal: AUD sell

As discussed in Dow and S&P 500 are all topping out, relative to risk barometer currency AUD (updated) and Asia is overpricing risk - Japan FX buying this is what happens when you buy into oversold assets. Since the AUD is the barometer of risk, with what happened in the last 2hrs (sell occurred prior to CPI data, yes insider info passed on to funds)

The point is longs have been decimated. 0.87 swing point is still on it's all sell.

The point is longs have been decimated. 0.87 swing point is still on it's all sell.

Monday, July 26, 2010

Chinese banks do not pass stress tests: 2010

"China's banks are facing serious default risks on more than one-fifth of the Rmb7,700bn ($1,135bn) they have lent to local governments across the country, according to senior Chinese officials. In a preliminary self-assessment, China's commercial banks have identified about Rmb1,550bn in questionable loans to local government financing vehicles - which are mostly used to fund regional infrastructure projects. .A senior official from the CBRC told the FT these loans would not necessarily all go bad but that the country's non-performing loan ratio would almost certainly "increase slightly" at the end of the year .Chinese banks lent a record Rmb9,600bn last year more than double the new loans issued in 2008."

From: FT 26th July 2010

From: FT 26th July 2010

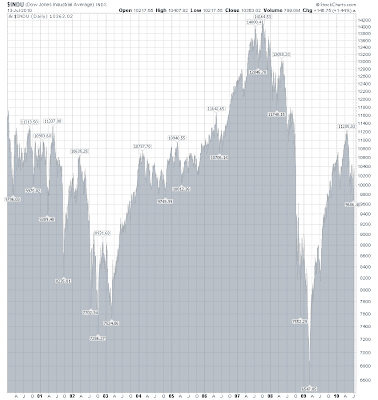

New highs for S/P 500 and Dow Jones 2010?

I don't think so, as discussed in Dow and S&P 500 are all topping out, relative to risk barometer currency AUD (updated) all major indices have now topped. The market has rallied on risk, namely from somewhat positive q2 earnings.

The rallies looked stretched on thin to medium volume accumulation. But if you look at the S&P 500 (10yr) and use the chart as example we can see how much liquidity can change markets and how the yield can also be sen as a indicator of stock trends; on the 5th October 2007 when the yield was at 3.78% the S&P 500 closed at 1,557.50 that was it's 10 yr peak, then as we all know the Fed cut rates and drove the yield down into 0% territory, on December the 2nd 2008 the yield was sitting below 0.01%, this yield remained when the index topped 1,205.90 (21st April 2010) it still remains at 0.01% with the current (26th July 2010) S&P 500 close at 1115.00. But, the S&P500 is still at 5yr lows compared to the 28th June 2005 close at 1201.50 when the yield was at 2.20%.

ref: Dynamic Yield Curve relative to S&P 500

The 10yr Dow chart (below) is self explanatory no new highs in the last 10yrs (apart from the 2008 price spike - before the bust) liquidity inflows or not:

The point? The deflationary argument may reiterate a strong tune in favour of deflationary forces on stocks prices, when liquidity still hasn't managed to propel stocks into 10 yr +highs. Also indicates that liquidity may not entirely move into the stocks, rather liquidity ended up supporting the broken balance sheets of the WHOLE global banking system.

The rallies looked stretched on thin to medium volume accumulation. But if you look at the S&P 500 (10yr) and use the chart as example we can see how much liquidity can change markets and how the yield can also be sen as a indicator of stock trends; on the 5th October 2007 when the yield was at 3.78% the S&P 500 closed at 1,557.50 that was it's 10 yr peak, then as we all know the Fed cut rates and drove the yield down into 0% territory, on December the 2nd 2008 the yield was sitting below 0.01%, this yield remained when the index topped 1,205.90 (21st April 2010) it still remains at 0.01% with the current (26th July 2010) S&P 500 close at 1115.00. But, the S&P500 is still at 5yr lows compared to the 28th June 2005 close at 1201.50 when the yield was at 2.20%.

ref: Dynamic Yield Curve relative to S&P 500

The 10yr Dow chart (below) is self explanatory no new highs in the last 10yrs (apart from the 2008 price spike - before the bust) liquidity inflows or not:

The point? The deflationary argument may reiterate a strong tune in favour of deflationary forces on stocks prices, when liquidity still hasn't managed to propel stocks into 10 yr +highs. Also indicates that liquidity may not entirely move into the stocks, rather liquidity ended up supporting the broken balance sheets of the WHOLE global banking system.

Thursday, July 22, 2010

Dow and S&P 500 are all topping out, relative to risk barometer currency AUD (updated)

We have a topped out in literally all markets

. The market has already factored in the bullshit '1 bank fail out of all EU banks' stress tests.

*update credibility coming online with EU bank stress tests - Spanish Banks fail (several). Watch for major selling on Europe's open

European 'officials' ECB and IMF, Germany Swiss, UK and the press will all argue about the validity of the results. Leading to volatility (watch LIBOR spreads) until the market rolls over with a fat sell signal.

So all eyes now to India and China with both power house economies slowing, especially India with balance of payments slowing into H2.

Also watch INR (India) and CNY (China) on FX depreciation which indicates that exports are slowing thus currencies adjusting to stay competitive (China's in a perpetual/artifical low adjustment); this should further put strain on the USD crosses (buy). Can be seen also in Oil/gold sells.

topped out charts (Dow, S&P 500) relative to the 'gauge' risk currency the AUD

Dow relative to AUD

S&P 500 relative to AUD

. The market has already factored in the bullshit '1 bank fail out of all EU banks' stress tests.

*update credibility coming online with EU bank stress tests - Spanish Banks fail (several). Watch for major selling on Europe's open

European 'officials' ECB and IMF, Germany Swiss, UK and the press will all argue about the validity of the results. Leading to volatility (watch LIBOR spreads) until the market rolls over with a fat sell signal.

So all eyes now to India and China with both power house economies slowing, especially India with balance of payments slowing into H2.

Also watch INR (India) and CNY (China) on FX depreciation which indicates that exports are slowing thus currencies adjusting to stay competitive (China's in a perpetual/artifical low adjustment); this should further put strain on the USD crosses (buy). Can be seen also in Oil/gold sells.

topped out charts (Dow, S&P 500) relative to the 'gauge' risk currency the AUD

Dow relative to AUD

S&P 500 relative to AUD

Tuesday, July 20, 2010

Asia is overpricing risk (update 2) - PboC now pricing in export collapse. CNY will drop, US/CHINA trade war coming soon...

"BEIJING--If China's export juggernaut falters, the country's central bank will allow its renminbi currency to fall against the U.S. dollar, thereby making Chinese goods cheaper overseas, a key monetary adviser here said.

Zhou Qiren, a member of the Monetary Policy Committee, an advisory body to the People's Bank of China, also told The Asahi Shimbun in an interview that Beijing's announcement June 19 that it would allow the renminbi to fluctuate more flexibly against the greenback starting June 21 should have been made much earlier.

Zhou said having a fixed exchange rate with the dollar over the past two years had been a burden for China.

The best way for China to reverse a sharp fall in exports would be to allow its currency to fall in value, too, he added.

No sooner had China announced its new policy than the renminbi began to rise in value against the dollar. In recent days, however, the rate has remained almost at the same level.

At the close of inter-bank trading on the Shanghai foreign exchange market Monday, the renminbi traded at 6.7780 yuan against the dollar, only up 0.71 percent since the June 19 announcement.

Chinese exports to both the United States and Europe had been surging until June. But there is now concern that exports will start falling"

Market is overpricing risk (update 5) - US/German/Swiss investment bank/s selling a lot of EUR

Nice reversal with a 1.30 cap (EUR/USD). Plus this rumor: huge selloff by funds in Eurostoxx futures @ 63,000 contracts.

There you go Asia (and anybody else...say Goldman Sachs). You bought a bull trap

There you go Asia (and anybody else...say Goldman Sachs). You bought a bull trap

Asia's 'planning' economies and their massive market intervetion (FX)

There is a lot talk about intervention/manipulation of the markets as discussed in: Manipulation of the market. Sinister design by the powers at be? Or just stupidities last gasp, it does occur but mostly in the Foreign Exchange markets where central banks/government have direct buy/sell into the market. Not stocks. This FX intervention predominantly occurs out of Asia. This has become in the last 3 months an almost paranoid and bizarre style of intervention. Namely the export countries such as South Korea, Japan, Taiwan and of course China.

China has been fixing various rates above their USD peg please refer to The PBoC are... and The PBoC are....(update 1) has been almost comical. Fixing rate, then buying USD to drop the 'fixed' Yuan rate against the US currency; happens daily. But it is Japan that is out of control with FX intervention, namely the BoJ. Japan is a political basket case, with a central bank that has an ingrained paranoia of YEN appreciation. Why? Their export markets. The same with South Korea, who intervene so often with the WON they (South Korea) might as well do what China did (and is still doing), and just peg the WON to the USD and be done with it, instead they (South Korean government passed legislation banning forward contracts of WON buy/sells please refer to: Amazing Central bank intervention (update 1)

The other comical aspect is the insane buying of the EUR in the last month/s (starting in May 2010); not only have all these countries mentioned carrying huge FX losses on the EUR; they also have huge reserves of USD that have depreciated. So if you buy (feverishly) EUR/USD then your USD reserves take a hit. So it works like this: Japan then sells YEN/USD goes up, South Korea then sells the WON /USD goes up, China then lets the Yuan appreciate the buys USD (thus USD appreciates against Yuan). Then they (countries mentioned) buy EUR and USD crosses (CAD, AUD, REAL etc) in a 'FX trader living in an asylum way'.

This goes on daily and as mentioned in the last 3 mths in a hyper way. The obvious answer to erratic central banks behavior is Asia's planning government/s are losing control of their fledgling export markets/political situations.

In other words Asia's export markets probably are about to collapse. Big time.

*please note revised post :The 2009 'Obama bounce' / liquidity rallies have come to an end. (*revised)

China has been fixing various rates above their USD peg please refer to The PBoC are... and The PBoC are....(update 1) has been almost comical. Fixing rate, then buying USD to drop the 'fixed' Yuan rate against the US currency; happens daily. But it is Japan that is out of control with FX intervention, namely the BoJ. Japan is a political basket case, with a central bank that has an ingrained paranoia of YEN appreciation. Why? Their export markets. The same with South Korea, who intervene so often with the WON they (South Korea) might as well do what China did (and is still doing), and just peg the WON to the USD and be done with it, instead they (South Korean government passed legislation banning forward contracts of WON buy/sells please refer to: Amazing Central bank intervention (update 1)

The other comical aspect is the insane buying of the EUR in the last month/s (starting in May 2010); not only have all these countries mentioned carrying huge FX losses on the EUR; they also have huge reserves of USD that have depreciated. So if you buy (feverishly) EUR/USD then your USD reserves take a hit. So it works like this: Japan then sells YEN/USD goes up, South Korea then sells the WON /USD goes up, China then lets the Yuan appreciate the buys USD (thus USD appreciates against Yuan). Then they (countries mentioned) buy EUR and USD crosses (CAD, AUD, REAL etc) in a 'FX trader living in an asylum way'.

This goes on daily and as mentioned in the last 3 mths in a hyper way. The obvious answer to erratic central banks behavior is Asia's planning government/s are losing control of their fledgling export markets/political situations.

In other words Asia's export markets probably are about to collapse. Big time.

*please note revised post :The 2009 'Obama bounce' / liquidity rallies have come to an end. (*revised)

Monday, July 19, 2010

Market is overpricing risk (update 4) - US/German/Swiss investment bank/s buying a lot of EUR

On the cusp of EU stress tests, this could indicate a massive sell at the 1.30 point v's USD, if EU stress tests fail to invigorate the market.

Or a mis-pricing of risk has spilled over to Western markets from an insane day (20th July 2010) of Asian risk buying particularly out of Japan and China

Or a mis-pricing of risk has spilled over to Western markets from an insane day (20th July 2010) of Asian risk buying particularly out of Japan and China

Asia is overpricing risk (update 1) - Japan and China have loss the plot

...they even ignored Chinese Chamber of Commerce saying H2 is going to be a horror show for Chinese exports.

But, BoJ/Japan political selling of the YEN which supported risk buys across the boards was the winner.

except for the Nikkei down -1.19%

This is desperation. Re: Japan

But, BoJ/Japan political selling of the YEN which supported risk buys across the boards was the winner.

except for the Nikkei down -1.19%

This is desperation. Re: Japan

Asia is overpricing risk - Japan FX buying

The Japanese have gone mad in trying to stabilize their YEN; Bank of Japan, Mega banks, Japanese housewife's made a feverish buy of their favorite currency: the Aussie as at 20 July 2010

refer:

this 'fever' style buying deserves to be punished....market 'tora, tora, tora' stylee

refer:

this 'fever' style buying deserves to be punished....market 'tora, tora, tora' stylee

The 2009 'Obama bounce' / liquidity rallies have come to an end. (*revised)

As discussed in US earnings - rallies markets into widening volatility, the perpetual bull run ran out of steam in January 2010. The arguments for a sustained bull run in stocks run from two perspectives 1. It was direct stimulus from governments that encouraged consumers to spend hence increasing confidence in the short /mid term (Housing positives) 2. Liquidity and volume; not to so much the average self funded trading but institutional trades that were funded by underwriting losses; the Federal Reserve was responsible for this, as was the Treasury/US government (TARP funds). To estimate how much money went into stocks to drive them up into 2009/10 highs (dow 2009/10 high @ 11205, S&P 500 2009/10 high @1219) would be on balance to the profits that were made (banks) - the main mover of stock rallies in 2009/2010. But, investment banks, retail banks, brokerage firms don't make money on trading alone. The 'other' way is to increase profit is with leverage trading especially with risk assets like housing, commercial property derivatives, M&A's; the other factor is at some-point banks have to start to consolidate toxic assets that they hold off balance sheets from 2009 onward. So in simple terms, we get moves in stocks from institutional buyers on large volume buys, retail/self funded traders then buy on confidence via government stimulus and rhetoric please refer top a 2009 blog post title How are the markets trading? Liquidity inflows? Green Shoots? Or market hysteria? which centers around the 'Obama bounce' rally in 2009.

The 2009 bull run in stocks was based on profitability of the banking sector, this may not occur in 2010; therefor stock rallies will not adjust to 2009/10 highs. To what extend the Federal Reserve will instigate more quantitative easing is disputable how much (this time) will flow into bank profits. This will effect investor sentiment in a negative manner.

In 2010 we have less liquidity in the market (check your volume indicators) and a lot of volatility. Smaller funded traders or 'dumb' money is still lingering in the market, and buying on the back of smart money selling on rallies; this is 'marked up' distribution. The earnings season for the US has been relatively disappointing with Bank of America, Citigroup, General Electric all reporting less then expected profits for the quarter. A seasoned analyst may look at why earnings have risen (banks) but net profits have declined, which could indicate that there is still asset deprecation on balance sheets sucking up profits.

All and all, it indicates that the rallies of 2009/10 have certainly come to end, are we currently sliding into a bear market? Not yet, what we have now is large swing volatility which is more of a bull trap for light volume 'dumb' trading; but the problem is anyone hedging with gold/some commodities to off set stock volatility will get the commodity price swings (on the downside) which is the China slowing down 'syndrome'. What is left is some fixed income trading of high yield assets, but that is just swing trading from high/lows and scalping profits.

Until we get a clear sign that the market is going to roll over into a large sell off; short selling will be a brave endeavor. Governments/central banks (if you want to talk about intervention etc) are holding off the short sellers on the EUR and this was done extremely well. The shorting will probably take place, as discussed in the post: China is about to crash: GDP q2 at 10.3% and falling of the commodity producing countries and their currencies. Should be some nice clear sells in the coming mouths.

The 2009 bull run in stocks was based on profitability of the banking sector, this may not occur in 2010; therefor stock rallies will not adjust to 2009/10 highs. To what extend the Federal Reserve will instigate more quantitative easing is disputable how much (this time) will flow into bank profits. This will effect investor sentiment in a negative manner.

In 2010 we have less liquidity in the market (check your volume indicators) and a lot of volatility. Smaller funded traders or 'dumb' money is still lingering in the market, and buying on the back of smart money selling on rallies; this is 'marked up' distribution. The earnings season for the US has been relatively disappointing with Bank of America, Citigroup, General Electric all reporting less then expected profits for the quarter. A seasoned analyst may look at why earnings have risen (banks) but net profits have declined, which could indicate that there is still asset deprecation on balance sheets sucking up profits.

All and all, it indicates that the rallies of 2009/10 have certainly come to end, are we currently sliding into a bear market? Not yet, what we have now is large swing volatility which is more of a bull trap for light volume 'dumb' trading; but the problem is anyone hedging with gold/some commodities to off set stock volatility will get the commodity price swings (on the downside) which is the China slowing down 'syndrome'. What is left is some fixed income trading of high yield assets, but that is just swing trading from high/lows and scalping profits.

Until we get a clear sign that the market is going to roll over into a large sell off; short selling will be a brave endeavor. Governments/central banks (if you want to talk about intervention etc) are holding off the short sellers on the EUR and this was done extremely well. The shorting will probably take place, as discussed in the post: China is about to crash: GDP q2 at 10.3% and falling of the commodity producing countries and their currencies. Should be some nice clear sells in the coming mouths.

Sunday, July 18, 2010

IMF looking for cash?

With a lot of 'smoke and mirrors' going on especially with the very nervous central banks of the world and countries particularly China (where transparency is a dirty word); the one thing the market eyes more than anything is funding problems , liquidity and credit problems (both interbank and inter-country). China's banks in the coming months will start to knock on the door of PBoC (People Bank of China) for cash, which would be a clear signal to the markets that China's property market has crashed. However Europe's liquidity problems have entered a uncertain phase, with the European Central Bank absorbing vast amounts of EU debt and commercial paper, more so from Spain. With both the IMF and EU denying more loans to Hungry refer to article: Markets braced for turmoil after IMF and EU withdraw £17bn Hungary financing dea

Now the International Monetary Fund (IMF) is asking is trying to raise capital to the sum of 1000billion. Short from creating their own money (as opposed to the ECB and Fed), the IMF can only sell it's gold (large chunk) as an attempt to re-capitalize:

"The spokesperson, however, declined to elaborate on how much the IMF will increase its lending resources."

Smells funny...

Article here

Now the International Monetary Fund (IMF) is asking is trying to raise capital to the sum of 1000billion. Short from creating their own money (as opposed to the ECB and Fed), the IMF can only sell it's gold (large chunk) as an attempt to re-capitalize:

"The spokesperson, however, declined to elaborate on how much the IMF will increase its lending resources."

Smells funny...

Article here

Wednesday, July 14, 2010

China is about to crash: GDP q2 at 10.3% and falling

So we have a 11.1% hit the wires, traders got confused with the H1 (11.1%) figure (the confusion was that they thought it was a surge over the 10.5% q2 figure y/y prior) and bought up risk assets (which were selling prior to the release); but then the figure of the current q2 10.3% hit the wires and it was back to selling again.

Then, we have some (small number) bring up the 'Goldilocks syndrome' for an economy, stable inflation/moderate growth; even a few traders from Shanghai (where else) saying the same.

Problem is the 'Goldilocks' call was made in 2006/07 on the US economy before it, well... you know what happened (US crashed in 2008)

Check this video report from CBS news, US in a 'Goldilocks' economy (2006/7)

A fucking omen.

Short position/s will start to light up, not so much in China; but Brazil/Australia/South Africa/Argentina/Canada: all over priced stock markets with high yield/s FX etc

Then, we have some (small number) bring up the 'Goldilocks syndrome' for an economy, stable inflation/moderate growth; even a few traders from Shanghai (where else) saying the same.

Problem is the 'Goldilocks' call was made in 2006/07 on the US economy before it, well... you know what happened (US crashed in 2008)

Check this video report from CBS news, US in a 'Goldilocks' economy (2006/7)

A fucking omen.

Short position/s will start to light up, not so much in China; but Brazil/Australia/South Africa/Argentina/Canada: all over priced stock markets with high yield/s FX etc

Tuesday, July 13, 2010

The low volume/high stock market conspiracy myth.

I am reading this a lot at the moment (yeah where else...the internet) and had a link sent to me re: low volume/high priced stock buying etc as a central bank manipulation tool.

There is no conspiracy here; simply (and if you lazy traders studied accumulation and distribution in volume/liquidity) institutional/s (smart money) sell stock 'dumb money' buys stock at high prices, thus pushes a stock price up/or index on low volume. So if there are double sellers to every buyer, that is the obvious bid/offer sign. It's called 'marked up' distribution.

It has happened very quickly in the last week of so, please refer to: US earnings - rallies markets into widening volatility post

Yes, Wall Street firms/banks/even central banks will encourage 'dumb' money to buy, the flip side is the Goldman Sachs of the world will then short/sell the stock at any given time. That is the raw reality of the markets. Not a conspiracy, it's just to make cash (Wall Street). Central banks try to build confidence and have unintended consequences that effect the market i.e retail trader and some mutual fund (dumb money) reads: 'everything ok!' headline the by ECB (especially the ECB) or the Fed.

It is not the 'plunge protection team' that doesn't exist, nor the central banks buying stocks to support markets with some shadowy desire to undermine other markets or something. If you believe that: paranoid delusions.

There is no conspiracy here; simply (and if you lazy traders studied accumulation and distribution in volume/liquidity) institutional/s (smart money) sell stock 'dumb money' buys stock at high prices, thus pushes a stock price up/or index on low volume. So if there are double sellers to every buyer, that is the obvious bid/offer sign. It's called 'marked up' distribution.

It has happened very quickly in the last week of so, please refer to: US earnings - rallies markets into widening volatility post

Yes, Wall Street firms/banks/even central banks will encourage 'dumb' money to buy, the flip side is the Goldman Sachs of the world will then short/sell the stock at any given time. That is the raw reality of the markets. Not a conspiracy, it's just to make cash (Wall Street). Central banks try to build confidence and have unintended consequences that effect the market i.e retail trader and some mutual fund (dumb money) reads: 'everything ok!' headline the by ECB (especially the ECB) or the Fed.

It is not the 'plunge protection team' that doesn't exist, nor the central banks buying stocks to support markets with some shadowy desire to undermine other markets or something. If you believe that: paranoid delusions.

South Korean unemployment up June 2010

A very good risk barometer to export confusion coming out of Asia. Which as we know feeds US consumption. US consumption down = Asian unemployment up (sans goverment stimulus)

"South Korea’s unemployment rate rose for the first time in five months in June as government employment programs began to wind down. The jobless rate climbed to 3.5 percent from 3.2 percent in May..."

from bloomberg

Remember South Korea ate into it's FX reserves to stablize the EUR in May 2010...not much of a cushion left.

"South Korea’s unemployment rate rose for the first time in five months in June as government employment programs began to wind down. The jobless rate climbed to 3.5 percent from 3.2 percent in May..."

from bloomberg

Remember South Korea ate into it's FX reserves to stablize the EUR in May 2010...not much of a cushion left.

US earnings - rallies markets into widening volatility

Some market watches have scratched the heads at the powerful rallies that taken place via US corporate earnings; more particularly from Alcoa and Intel. As opposed to locking in a economic slowdown thus effecting stocks prices. What we have in simple terms is volatility in stocks (which were slightly oversold prior to US earnings), any intervention by central banks (Greek/Spain bond and C.paper buying by the ECB) and over hyped estimates by company CEO's. Will effect stock prices on the upside and encourage smaller investors to buy. So fund managers have gotten all excited at the possibility of a sustained bull run in stocks, some even referring to Bill Gross (PIMCO) now switching to stocks after believing the bond market bull run is finishing up. This is all based on the liquidity theory of sustained rallies into a bull run. It is an inflationary scenario based on excess liquidity. Which is a long term possibility, but currently confidence rallies on thin liquidity is the obvious factor. Please refer to Manipulation of the market. Sinister design by the powers at be? Or just stupidities last gasp

These markets, with high volatility/CB intervention, are very hard to make money in; unless you are using options/warrants/other derivatives at a high leverage and trade volatility.

The dow (using chart as an example) bull run ended on 20th Jan 2010 when the it completely dropped out of it's tight range it then subsequently collapsed to 9904 on the 8th of February 2010 then rallied to highs of 11258 on the 26th April 2010; a clearly unstained rally that then collapses to 9810 on the 7th June 2010. The recent 'U-Turn' rally on the 2 July 2010 form a low of 9659 to it's last close of 10362 indicates the widening trading ranges (refer to chart)

Short sellers will struggle to gain a clear sell in a supported/volatile market. Swing traders/ volatility trading will see some gain, but albeit small (unless you have leveraged up your delta risk at a higher % and moving a lot of money around).

We won't see sustained rallies in 2010 or 2011; because the reverse situation (as opposed to the synchronized rallies of 2009) is when Europe/US appears to be improving (and appearances are of course deceiving), China then hits us with the slow down spectra (as the train slows down it may jolt and fall of it's tracks i.e China crash); this counter relation of economic uncertainty will continue thus adding to market volatility.

Note: bull run that finished in Jan 20th 2010 (tight ranges blue/red line)

Note: Current widening/volatility range

These markets, with high volatility/CB intervention, are very hard to make money in; unless you are using options/warrants/other derivatives at a high leverage and trade volatility.

The dow (using chart as an example) bull run ended on 20th Jan 2010 when the it completely dropped out of it's tight range it then subsequently collapsed to 9904 on the 8th of February 2010 then rallied to highs of 11258 on the 26th April 2010; a clearly unstained rally that then collapses to 9810 on the 7th June 2010. The recent 'U-Turn' rally on the 2 July 2010 form a low of 9659 to it's last close of 10362 indicates the widening trading ranges (refer to chart)

Short sellers will struggle to gain a clear sell in a supported/volatile market. Swing traders/ volatility trading will see some gain, but albeit small (unless you have leveraged up your delta risk at a higher % and moving a lot of money around).

We won't see sustained rallies in 2010 or 2011; because the reverse situation (as opposed to the synchronized rallies of 2009) is when Europe/US appears to be improving (and appearances are of course deceiving), China then hits us with the slow down spectra (as the train slows down it may jolt and fall of it's tracks i.e China crash); this counter relation of economic uncertainty will continue thus adding to market volatility.

Note: bull run that finished in Jan 20th 2010 (tight ranges blue/red line)

Note: Current widening/volatility range

Monday, July 12, 2010

Trichet (ECB chief) on rating agency's

"PARIS, July 13 (Reuters) - The world needs more than three major credit ratings agencies because their actions exacerbate market swings, European Central Bank President Jean-Claude Trichet was quoted on Tuesday as saying.

'The ratings agencies in general tend to amplify rises and falls in financial markets. You can see it still today very visibly. That goes against financial stability,' he said in an interview with French daily Liberation.

'It is probably appropriate not to continue to have a worldwide oligopoly of three agencies. But the underlying issue is to attenuate or cancel out this amplification to which the rating agencies contribute.'

from here

What an idiot.

It's the ECB clandestine operations that are destabilizating markets. How? They (ECB) are buying poor quality sovergin debt and buying the EUR. The ECB is becoming a huge toxic waste dump.

Sunday, July 11, 2010

50/200 MA 'Death Cross' in effect: AUD

Yes, not only is the Dow showing a 50MA/200MA death cross (50day average passes under the 200 day average)

But the currency that is one of the biggest risk trades: the AUD is showing you a true death cross refer to charts:

daily (blue line 50MA, purple line 200MA)

daily zoomed out (black line 50MA, purple line 200MA)

But the currency that is one of the biggest risk trades: the AUD is showing you a true death cross refer to charts:

daily (blue line 50MA, purple line 200MA)

daily zoomed out (black line 50MA, purple line 200MA)

A liquidity Sh*t storm is brewing: and it's brutal (NYT link)

When banks and government/s make a mad rush to roll over debt and refinance through the ECB and bond markets; this all point to one thing, money is in short supply and the question will be who gets favored for a 'roll over'? Banks or government? This just means liquidity will be sucked out of the macro economy via higher funding costs ( passed on by banks) ,which means we will all be paying more for finance, which means expansion/recovery get's KO'ed, and if a trillion dollar liquidity crunch is the number and the epicenter is Europe: a huge shitstorm is brewing (using China as they final smack-down)

"Their concern is that banks hungry for refinancing will compete with governments — which also must roll over huge sums — for the bond market’s favor. As a result, credit for business and consumers could become more costly and scarce, with unpleasant consequences for economic growth.

“There is a cliff we are racing toward — it’s huge,” said Richard Barwell, an economist at Royal Bank of Scotland and formerly a senior economist at the Bank of England, Britain’s central bank. “No one seems to be talking about it that much.” But, he added, “it’s of first-order importance for lending and output.”

Banks worldwide owe nearly $5 trillion to bondholders and other creditors that will come due through 2012, according to estimates by the Bank for International Settlements. About $2.6 trillion of the liabilities are in Europe."

from: NYT 11th July 2010

"Their concern is that banks hungry for refinancing will compete with governments — which also must roll over huge sums — for the bond market’s favor. As a result, credit for business and consumers could become more costly and scarce, with unpleasant consequences for economic growth.

“There is a cliff we are racing toward — it’s huge,” said Richard Barwell, an economist at Royal Bank of Scotland and formerly a senior economist at the Bank of England, Britain’s central bank. “No one seems to be talking about it that much.” But, he added, “it’s of first-order importance for lending and output.”

Banks worldwide owe nearly $5 trillion to bondholders and other creditors that will come due through 2012, according to estimates by the Bank for International Settlements. About $2.6 trillion of the liabilities are in Europe."

from: NYT 11th July 2010

Secret gold swap - a panic in disgiuse ECB? Or is a country in trouble?

"...the day after original reports about the swaps, BIS emailed a statement saying that the swaps had not been conducted with monetary authorities but purely with commercial banks.

This did nothing to quell the sense of mystery surrounding the deal or deals. It is almost inconceivable that a single commercial bank could have accumulated so much gold alone. And cynics have suggested that the whole affair still looks like a secretive European bailout that a single country wants to keep quiet.

In this case, one or more of the so-called bullion banks – which act as wholesale market-makers and include Goldman Sachs, Deutsche Bank, JP Morgan, HSBC, Barclays, UBS, Societe Generale, Mitsui and the Bank of Nova Scotia – would have agreed to act on behalf of a monetary authority"

Telegraph 11 July 2010

Whilst we are on that topic of central bank panic/intervention/last gasp manipulation

Manipulation of the market. Sinister design by the powers at be? Or just stupidities last gasp

Manipulation and/or direct intervention by goverment/central banks of the market happens constantly, if you didn't release this it would be probably be sensible you don't trade in the markets. The question is how widespread, how significant and how sinister is this manipulation?

On May 20th 2010 after the ECB/EU/IMF meetings a decision was made to protect the Euro; as it was under selling attack by short sellers namely hedge funds. The French president Nicholas Sakozy issued a warning that the Euro would be protected at all costs and that any down selling will be reversed very quickly. He was right, if fact refer to: Amazing Central Bank intervention (FX markets) the most obvious intervention or manipulation (where short sellers were forced to buy back short positions) by government and central banks (European central bank) took place on 20th of May 2010. It was a broad intervention/manipulation of the market on three fronts occurred by three central banks the Bank of Japan (sold USD), Reserve Bank of Australia (bought AUD - as the AUD is a risk barometer to market panic so it was bought and stabilized) and the European Central Bank/IMF drew a line under the EUR at 1.20. This was an extremely successful intervention and manipulation of traders who were buying and selling risk averse currencies. That is how it is, blatant and obvious and in some way acceptable (unfortunately); as long as central banks have a direct influence into the markets, as traders we have to factor in and accept their (again unfortunate) presence.

Of late there has been talk or rumours on the wires that the Swiss National Bank are now sitting of a huge amount of unrealized losses from it's EUR buying intervention (via ECB instructions). These rumours to me sound like traders possibly Hedge funds using counter tactics or fear to unsettle the markets due to it's recent stabilization (Europe, EUR etc). The other rumour is the ECB has accumulated so much toxic waste that it may have trouble reselling into back into the market (massive unrealized losses). So for the market looking to cut risk and sell from institutional investors/traders to the everyday person; they all know deep down that the propaganda won't stick much longer (central banks/government looking desperate), then the charade cannot be kept up for much longer and we have regained a selling momentum.

Stock manipulation or intervention is rarer as opposed to FX manipulation by Central banks/governments and there has been some talk that current Wall Street rallies have been bolstered by Federal Reserve bank buying via wall Street firms (the Plunge Protection team myth). There is no doubt that manipulation of stocks, FX/derivatives takes place, but the argument is that with thinning volumes and buying signal spikes point to a degree of manipulating of intervention by Central Banks/movement (PPT myth) is unlikely. What I do believe has taken place in the last month June 2010 and the last 2 weeks of July 2010 is that the only ammunition that government and central banks have left is what falling powers, leaders and empires have been trying to do in the dying moments are social/economic decline; is to try and manipulate the masses or market via rhetoric. Governments will attempt to re-seduce the people, central banks/governments will attempt to re-instill confidence into the market place/economy. As discussed in Pricing in the big one (sell) 2010 the market can be tricked on the short term, but on medium term to longer term it can't be; the massive amount of intervention that took place on the 20 May 2010 (and there after), via every central banks in the world is a short term trick or attempt at re-instilling confidence. The governments (and they are currently struggling with this) is to try and convince the people that 2009 was not a fluke (economic and social stabilization, even though underneath rot was setting in refer to:the EU/PIIGS, UK and even China re: wage hikes and strikes). So an attempt to fool the people again is hard, The Roman Empire couldn't do it, Napoleon tried it a second time and got so far and flopped, Germany during the last stages of WW2, Communist Europe after the Berlin Wall came down etc. One of the most comical ones and more recent is the Iraq war or invasion by the US army, when the Iraqi communication leader Mohammed Said al-Sahhaf, made hilarious statements to news reporters that they (Iraq army) had "... destroyed 2 tanks, fighter planes, 2 helicopters and their shovels - We have driven them back." and the "God will roast their stomachs in hell at the hands of Iraqis "all this was said whilst US tanks were driving up main Baghdad streets (refer to older blog post) .

So manipulation and intervention most certainly occurs in the markets and everyday life; but there is no sinister conspiracy theory attached or hidden agenda; simply fools are trying to maintain power and it is slipping. History shows that everything peaks out and then goes into a decline, nothing stays linear or constant; in the last stages of even the greatest Empires such as the Roman empire, stupidity, panic and disorder set in and then implodes. No shadowy figures, or ulterior motives just fools acting like fools until it all comes down. That's the reality.

Side note: re thinning volume and buys on stock positions/indices.

As the money flow indicators such as the On Balance Volume indicator show is that the smart money has been withdrawn and the 'dumb' money moved in buying stocks that most probably are bought at multiplied prices to their demand (or value). In other words 'confidence building' or short term manipulation' of everyday investors, say individual investors, has occurred. But as I said, this is a good example of mid to long term realization that all is not that good. So the 'dumb' money (eventually) will be pulled out as with the smart money.

On May 20th 2010 after the ECB/EU/IMF meetings a decision was made to protect the Euro; as it was under selling attack by short sellers namely hedge funds. The French president Nicholas Sakozy issued a warning that the Euro would be protected at all costs and that any down selling will be reversed very quickly. He was right, if fact refer to: Amazing Central Bank intervention (FX markets) the most obvious intervention or manipulation (where short sellers were forced to buy back short positions) by government and central banks (European central bank) took place on 20th of May 2010. It was a broad intervention/manipulation of the market on three fronts occurred by three central banks the Bank of Japan (sold USD), Reserve Bank of Australia (bought AUD - as the AUD is a risk barometer to market panic so it was bought and stabilized) and the European Central Bank/IMF drew a line under the EUR at 1.20. This was an extremely successful intervention and manipulation of traders who were buying and selling risk averse currencies. That is how it is, blatant and obvious and in some way acceptable (unfortunately); as long as central banks have a direct influence into the markets, as traders we have to factor in and accept their (again unfortunate) presence.

Of late there has been talk or rumours on the wires that the Swiss National Bank are now sitting of a huge amount of unrealized losses from it's EUR buying intervention (via ECB instructions). These rumours to me sound like traders possibly Hedge funds using counter tactics or fear to unsettle the markets due to it's recent stabilization (Europe, EUR etc). The other rumour is the ECB has accumulated so much toxic waste that it may have trouble reselling into back into the market (massive unrealized losses). So for the market looking to cut risk and sell from institutional investors/traders to the everyday person; they all know deep down that the propaganda won't stick much longer (central banks/government looking desperate), then the charade cannot be kept up for much longer and we have regained a selling momentum.

Stock manipulation or intervention is rarer as opposed to FX manipulation by Central banks/governments and there has been some talk that current Wall Street rallies have been bolstered by Federal Reserve bank buying via wall Street firms (the Plunge Protection team myth). There is no doubt that manipulation of stocks, FX/derivatives takes place, but the argument is that with thinning volumes and buying signal spikes point to a degree of manipulating of intervention by Central Banks/movement (PPT myth) is unlikely. What I do believe has taken place in the last month June 2010 and the last 2 weeks of July 2010 is that the only ammunition that government and central banks have left is what falling powers, leaders and empires have been trying to do in the dying moments are social/economic decline; is to try and manipulate the masses or market via rhetoric. Governments will attempt to re-seduce the people, central banks/governments will attempt to re-instill confidence into the market place/economy. As discussed in Pricing in the big one (sell) 2010 the market can be tricked on the short term, but on medium term to longer term it can't be; the massive amount of intervention that took place on the 20 May 2010 (and there after), via every central banks in the world is a short term trick or attempt at re-instilling confidence. The governments (and they are currently struggling with this) is to try and convince the people that 2009 was not a fluke (economic and social stabilization, even though underneath rot was setting in refer to:the EU/PIIGS, UK and even China re: wage hikes and strikes). So an attempt to fool the people again is hard, The Roman Empire couldn't do it, Napoleon tried it a second time and got so far and flopped, Germany during the last stages of WW2, Communist Europe after the Berlin Wall came down etc. One of the most comical ones and more recent is the Iraq war or invasion by the US army, when the Iraqi communication leader Mohammed Said al-Sahhaf, made hilarious statements to news reporters that they (Iraq army) had "... destroyed 2 tanks, fighter planes, 2 helicopters and their shovels - We have driven them back." and the "God will roast their stomachs in hell at the hands of Iraqis "all this was said whilst US tanks were driving up main Baghdad streets (refer to older blog post) .

So manipulation and intervention most certainly occurs in the markets and everyday life; but there is no sinister conspiracy theory attached or hidden agenda; simply fools are trying to maintain power and it is slipping. History shows that everything peaks out and then goes into a decline, nothing stays linear or constant; in the last stages of even the greatest Empires such as the Roman empire, stupidity, panic and disorder set in and then implodes. No shadowy figures, or ulterior motives just fools acting like fools until it all comes down. That's the reality.

Side note: re thinning volume and buys on stock positions/indices.

As the money flow indicators such as the On Balance Volume indicator show is that the smart money has been withdrawn and the 'dumb' money moved in buying stocks that most probably are bought at multiplied prices to their demand (or value). In other words 'confidence building' or short term manipulation' of everyday investors, say individual investors, has occurred. But as I said, this is a good example of mid to long term realization that all is not that good. So the 'dumb' money (eventually) will be pulled out as with the smart money.

Thursday, July 8, 2010

Dow rallies 6th, 7th, 8th (July 2010)

After 3 days of rallies 6th, 7th, 8th (July 2010) a bull trap has formed.

Note:

Thin volumes/OBV divergence

MFI flat to inverse at 39.05

Accumulation Distribution indicator divergence over dow price (overlay line)

sell signals within pivot point support ranges (refer to chart)

* MEC.research doesn't give investment advice, trade at your own risk

Note:

Thin volumes/OBV divergence

MFI flat to inverse at 39.05

Accumulation Distribution indicator divergence over dow price (overlay line)

sell signals within pivot point support ranges (refer to chart)

* MEC.research doesn't give investment advice, trade at your own risk

Could China end up in a liquidity 'Sh*t Storm'? (update 1)

The funniest thing, the current Australian (well not the people) goverment dismissed it's ex-leader within 24hrs on the 24 June 2010; on the premise that the 40% resources tax was a re-election death. So they ( Labor's current leader Julia Gillard) comprised with the miners an almost laughable tax concession (pegged to the 10yr Aust bond). I am not into over taxing business/companies but a public orientated 'rent tax' on overinflated miners is not such a bad thing, especially when Australia is looking down a gapping 58billion dollar fiscal deficit that will grow into 2011 (double dip recession/China slow down)

Whether the 'poll' backlash (former Labor leader) was against the mining tax is disputable. Still China was brought into the picture with medium/larger miners claiming China will look elsewhere for commodities. But as some analysts noted a 'resourse tax' was invetible especially as financing conditions (commodity producing countries) tighten and deficits will be a challenge to bring back into surplus.

China has just implicated a resource tax which will encompasses ALL of China's mining sector/s. (that's the funny/ironic part)

this indicates three things:

*Credit revenue form exports are slowing

*Liquidity conditions for local/region councils are being squeezed

*Liquidity and financing for China is drying up

Whether the 'poll' backlash (former Labor leader) was against the mining tax is disputable. Still China was brought into the picture with medium/larger miners claiming China will look elsewhere for commodities. But as some analysts noted a 'resourse tax' was invetible especially as financing conditions (commodity producing countries) tighten and deficits will be a challenge to bring back into surplus.

China has just implicated a resource tax which will encompasses ALL of China's mining sector/s. (that's the funny/ironic part)

this indicates three things:

*Credit revenue form exports are slowing

*Liquidity conditions for local/region councils are being squeezed

*Liquidity and financing for China is drying up

Creative Destruction blog

A new sub-blog called Creative Destruction will replace the popular culture/fashion/art/film/books comics/sex and violence on MEC research. Instead MEC research will focus solely on the markets, as things are getting rather tasty (economically speaking).

New blog: Creative Destruction

New blog: Creative Destruction

Wednesday, July 7, 2010

"German May Current Acct Surplus EUR2.2B Vs EUR11.3B In April"...Nasty

"FRANKFURT (Dow Jones)--The German current account surplus fell sharply to EUR2.2 billion in May from April, as a 14.8% rise in imports outpaced a 9.2% rise in exports, the Federal Statistics Office Destatis said Thursday.

At a seasonally-adjustd EUR80.8 billion, exports from Europe's largest economy were thus up 28.8% from a year earlier and at their highest since 2007, the strongest year-on-year increase in 10 years, Destatis said.

Imports also rose to their highest level in over a year and a half, however, reducing the merchandise trade surplus to EUR9.7 billion from EUR13.1 billion in April.

The balance in services also swung to a deficit of EUR1.5 billion from a surplus of EUR300 million in April, while the balance in investment income swung to a deficit of EUR3.2 billion from an EUR800 million surplus"

And the IMF/ECB/FED/Obama and everyone else expects Germany to agree to higher inflation rates to 'boost' the global economy rather than austerity measures to reign in debt?

I don't think so and nor does Germany after this data. Inflation signs are already there (consumption up on imports over exports).AUD swing point sell activated

We currently have confidence rallies in all markets, except the USD.

Australian unemployment figures came out with a 45,900 extra jobs added (8 July 2010). A politically designed uplift via the government statisticians (ABS) in ready for elections in 2010 (although politically a risky play, because of it's bullshit figure). This caused the Japanese spec buyers to pile on more longs. Sustainable? Not at all, refer to The currency hit list: The Australian dollar (update 1) when Australian consumption is directly linked to an overinflated housing market (equity draw-downs) the so called Australian 'economic cushion' (from European debt crisis/China slowdown) is illusionary.

In summary, sharp corrective plays (property, capital expenditure, banks/lending rates/write-downs/loan provisions/mining/retail and finally 'realistic' unemployment numbers) should now occur within the Australian economy in the next 6mths.

First being the AUD correction with a 0.87 swing point (on a monthly chart) now activated.

Australian unemployment figures came out with a 45,900 extra jobs added (8 July 2010). A politically designed uplift via the government statisticians (ABS) in ready for elections in 2010 (although politically a risky play, because of it's bullshit figure). This caused the Japanese spec buyers to pile on more longs. Sustainable? Not at all, refer to The currency hit list: The Australian dollar (update 1) when Australian consumption is directly linked to an overinflated housing market (equity draw-downs) the so called Australian 'economic cushion' (from European debt crisis/China slowdown) is illusionary.

In summary, sharp corrective plays (property, capital expenditure, banks/lending rates/write-downs/loan provisions/mining/retail and finally 'realistic' unemployment numbers) should now occur within the Australian economy in the next 6mths.

First being the AUD correction with a 0.87 swing point (on a monthly chart) now activated.

Relief rally on the Dow 10,000 resistance breached

Markets rallied across the board on the 7th July 2010. Reasons why for relief rally:

* Eurozone Q1 confirmed at +0.2% q/q, +0.6% y/y vs prev +0.2%/0.5%. As Exp

* German May Industrial Orders -0.5% m/m vs prev +3.2%. +0.5% Exp

* UK June BRC shop price index +1.5% y/y, May +1.8%

* EU Commission: Greek reform programme broadly on track

* Fed"s Fisher: Fed has "done enough" asset purchasing; have not seen European

contagion, but is always a risk; big bank shave too much concentration of power,

not healthy (CNBC)

* European bank stress tests will include 16-17% haircut on Greek bonds (Reuters

banking sources)

* Germany"s Merkel: EUR has stabilized, on stronger foundation than pre-crisis

* Irish Fin Ministry: Sees 2010 GDP +1%; Funding position comfortable for year

* EU Stress Test: Adverse scenario assumes 3 pct point variation of GDP from

forecasts; Scenarios include sovereign risk shock comparable to early May 2010

markets; Results to be disclosed in total and bank-by-bank July 23 (Cebs doc)

* Nikkei News: Exporters likely to shift EUR/JPY forecasts to 110-115

* Greek lawmakers agree in principle on pension reform in preliminary parl. Vote

* Fed Kocherlakota: reiterates call for US bank tax to fund possible future

bailout, capital cushions problematic

* Pres. Obama names Export Council appointments, council will focus on doubling

exports over next 5 years, Obama urges level playing field with China

* Fed Hoenig: favors 1% target, lowered exp. of growth to 3% for next year

* State Street: will report earning well above analysts forecasts as company has

seen revenue trends improve

* EIA: raised forecasts for world oil demand

A mixed bag of semi positive rhetoric and assumptions (will State Street deliver the 0.92 over the 0.72 earnings per share?).

In other words a nice 'bull trap' forming.

* Eurozone Q1 confirmed at +0.2% q/q, +0.6% y/y vs prev +0.2%/0.5%. As Exp

* German May Industrial Orders -0.5% m/m vs prev +3.2%. +0.5% Exp

* UK June BRC shop price index +1.5% y/y, May +1.8%

* EU Commission: Greek reform programme broadly on track

* Fed"s Fisher: Fed has "done enough" asset purchasing; have not seen European

contagion, but is always a risk; big bank shave too much concentration of power,

not healthy (CNBC)

* European bank stress tests will include 16-17% haircut on Greek bonds (Reuters

banking sources)

* Germany"s Merkel: EUR has stabilized, on stronger foundation than pre-crisis

* Irish Fin Ministry: Sees 2010 GDP +1%; Funding position comfortable for year

* EU Stress Test: Adverse scenario assumes 3 pct point variation of GDP from

forecasts; Scenarios include sovereign risk shock comparable to early May 2010

markets; Results to be disclosed in total and bank-by-bank July 23 (Cebs doc)

* Nikkei News: Exporters likely to shift EUR/JPY forecasts to 110-115

* Greek lawmakers agree in principle on pension reform in preliminary parl. Vote

* Fed Kocherlakota: reiterates call for US bank tax to fund possible future

bailout, capital cushions problematic

* Pres. Obama names Export Council appointments, council will focus on doubling

exports over next 5 years, Obama urges level playing field with China

* Fed Hoenig: favors 1% target, lowered exp. of growth to 3% for next year

* State Street: will report earning well above analysts forecasts as company has

seen revenue trends improve

* EIA: raised forecasts for world oil demand

A mixed bag of semi positive rhetoric and assumptions (will State Street deliver the 0.92 over the 0.72 earnings per share?).

In other words a nice 'bull trap' forming.

Monday, July 5, 2010

Weird China/Aust trade numbers

Aust term of trade came out with May 2010 surplus of 1.65billion mostly from these:

Yet China iron ore (and I imagine coke, coal and briquettes all fell off from higher demand i.e to smolder the iron ore) down in June 2010:

"SHANGHAI, June 11 -- China's iron ore imports fell 6 percent to 51.9 million tonnes in May from the previous month, while steel product exports rose 15 percent from April.

Iron ore imports were 3 percent lower from a year earlier, but took the year-to-date imports to 262 million tonnes, up 8.4 percent versus a year earlier, Chinese customs said on Thursday.

Iron ore imports have started to fall after hitting an annual record of 59 million tonnes in March, while stagnant steel prices and possible large cutbacks in steel mill production could further squeeze imports over next few months.

"Most of the deals were signed in March or early April when prices were still high and buying was active, but orders have dramatically fallen in May after prices plummeted," said an iron ore trader based in Ningbo.

"The Indian monsoon will also have a big impact on iron ore imports in the summer."

Spot iron ore prices slumped by more than 25 percent from the all-time high of around $200 per tonne in late April.

Smaller Chinese steel mills and traders have spurned imported ore amid fluctuating steel prices as uncertainties in steel demand have continued to weigh on the market.

Imports are expected to fall sharply in June after a few Chinese steel mills brought forward maintenance plans to cut output as steel consumption by downstream sectors is expected to fall in the next few months."from Reuters

ABS are cooking up a large trade surplus here...

To blindside the market to Australia's time-bomb housing bubble?

- coal, coke and briquettes, up $329m (10%)

- metal ores and minerals, up $157m (3%)

Yet China iron ore (and I imagine coke, coal and briquettes all fell off from higher demand i.e to smolder the iron ore) down in June 2010:

"SHANGHAI, June 11 -- China's iron ore imports fell 6 percent to 51.9 million tonnes in May from the previous month, while steel product exports rose 15 percent from April.

Iron ore imports were 3 percent lower from a year earlier, but took the year-to-date imports to 262 million tonnes, up 8.4 percent versus a year earlier, Chinese customs said on Thursday.

Iron ore imports have started to fall after hitting an annual record of 59 million tonnes in March, while stagnant steel prices and possible large cutbacks in steel mill production could further squeeze imports over next few months.

"Most of the deals were signed in March or early April when prices were still high and buying was active, but orders have dramatically fallen in May after prices plummeted," said an iron ore trader based in Ningbo.

"The Indian monsoon will also have a big impact on iron ore imports in the summer."

Spot iron ore prices slumped by more than 25 percent from the all-time high of around $200 per tonne in late April.

Smaller Chinese steel mills and traders have spurned imported ore amid fluctuating steel prices as uncertainties in steel demand have continued to weigh on the market.

Imports are expected to fall sharply in June after a few Chinese steel mills brought forward maintenance plans to cut output as steel consumption by downstream sectors is expected to fall in the next few months."from Reuters

ABS are cooking up a large trade surplus here...

To blindside the market to Australia's time-bomb housing bubble?

Could China end up in a liquidity sh*t storm?

A reported 100 billion dollar infrastructure project/s in western China? Were are they going to get the money from? Since the Yuan is beginning to appreciate, or is it? Of will they (China) sell off their huge FX reserves?

Remember China's Agbank couldn't secure funding for a final IPO push

All points to ominous Chinese liquidity problems.

Remember China's Agbank couldn't secure funding for a final IPO push

All points to ominous Chinese liquidity problems.

The currency hit list - The Australian Dollar (update 1)

The global ecomomy is becoming a basket case, the L shaped recovery, or economic drag on subpar growth will continue, at this point, indefinitely. The huge amount of stimulus and bailouts and monetary intervention by central banks has failed. Why? Well look at European and the interconnected banking sector that has linked it's self all to decayed assets via Europe's messy economies: the PIIGS. Forcing bonds yields up, CDS/LIBOR spreads to widen, it's either costing banks more to hold crap assets or destroying the value of assets. It summary the Euro zone is a massive risk contagion and stimulus/monetary efforts either exacerbated this or covered it up, now it's pay day. The European Central Bank under Jean-Claude Trichet have not only ran out of options (I guess they ECB could make a huge leveraged bet that Greece will return to profit via massive olive oil sales), but now hold billions of Euro's in unrealized losses as it tries to unclog the sentiment of fear in the European banking sector. But as Europe moves further into austerity, the slow down and the depreciated, or 'toxic assets will increase'. The Euro zone (unfortunately) is a write off.

So, Asia will be effected as a slowdown in the global economy takes place, if measured by GDP, a 'double dip recession' is a certainty. The problems in Asia is of course funding costs via banks and lenders, it must be made clear that although Asian banks may not have entangled themselves with complex derivatives, they are becoming more risk orientated as (particularly China, Taiwan, Hong Kong and South Korea) have allowed extra leverage into the economies with the consumer speculating heavily into property. If bank funding does blow out or a 'Lehman Brothers' incident occurs somewhere (we shouldn't rule out that fact that the commercial property markets have been quite but there are write-downs ahead); will send interbank funding spreads to 2008 levels .

Asian countries that have over leveraged particularly in housing are going to be very vulnerable to a global double dip recession. Australia (Asian region) is number 1 risk problem in that sense.

Politically, in a global sense, there are now the beginnings of 'fear and loathing'. In Australia the center left party (Labor) dismissed their leader (Australian prime minister at the time) in less than 24hrs. Kevin Rudd was not even voted out by the people, rather quickly removed from office (by his own party) and replaced . He (Rudd) is actually responsible for re-inflating the Australian housing market and skirting Australia from entering into a full blown recession/depression in 2008/2009. This was done by maintaining consumption via equity and wealth effect from housing. The Australian exports markets never really returned to 2007 levels (after 2008 Lehman collapse). The political dismissal centered around a paranoid delusive aspect of voter backlash from the goverments proposed 40% mining tax; this may have been a primer, but dissatisfaction runs deeper. As fears of Australia's vulnerability to falling Asian import markets (Australian raw material), goverment deficits, inflation and over leveraged housing may also been a unsettling dilemma for Australian voters. The point being is although the new prime minister Julia Gillard has now allowed miners a free ride by attaching the mining tax to the 10yr Aussie bond (it falls, so does the tax threshold). The big questions is when Australian begins to slow down, and this should be a rapid decent into the last 6mths of 2010. Will the new prime minster and her party initiate a 2nd round of stimulus? Since the budget deficit for Australia is 56+billion (for a population 21million - a tax receipt short fall from hell) if she does and sends the Australian deficit further into the red, no doubt the Aussie bond yields will go upward and bond vigilantes will start to look at Australia and price in higher yield offerings; thus effecting Australia's credit rating (such as the European PIIGS)

What is left is the high yielding Australian dollar, whilst we have deprecating currencies global, the AUD has been bought for it's high yield and desirability for Japanese carry traders. In 2008 I successful held a put on the AUD refer to AUD put 2010. It was my "go for the jugular" George Soros moment, admittedly the return was (very) micro compared to his "1billion dollars" in one day betting against the GBP ( UK pound) in 1992. Still in 2010 we have have a another 'jugular moment' brewing for the AUD as the Reserve Bank of Australia will start to cut rates in the next 6mths.

refer to chart AUD/USD:

the support (breach) is 0.80

a swing point (monthly chart) down at 0.87.

So, Asia will be effected as a slowdown in the global economy takes place, if measured by GDP, a 'double dip recession' is a certainty. The problems in Asia is of course funding costs via banks and lenders, it must be made clear that although Asian banks may not have entangled themselves with complex derivatives, they are becoming more risk orientated as (particularly China, Taiwan, Hong Kong and South Korea) have allowed extra leverage into the economies with the consumer speculating heavily into property. If bank funding does blow out or a 'Lehman Brothers' incident occurs somewhere (we shouldn't rule out that fact that the commercial property markets have been quite but there are write-downs ahead); will send interbank funding spreads to 2008 levels .

Asian countries that have over leveraged particularly in housing are going to be very vulnerable to a global double dip recession. Australia (Asian region) is number 1 risk problem in that sense.

Politically, in a global sense, there are now the beginnings of 'fear and loathing'. In Australia the center left party (Labor) dismissed their leader (Australian prime minister at the time) in less than 24hrs. Kevin Rudd was not even voted out by the people, rather quickly removed from office (by his own party) and replaced . He (Rudd) is actually responsible for re-inflating the Australian housing market and skirting Australia from entering into a full blown recession/depression in 2008/2009. This was done by maintaining consumption via equity and wealth effect from housing. The Australian exports markets never really returned to 2007 levels (after 2008 Lehman collapse). The political dismissal centered around a paranoid delusive aspect of voter backlash from the goverments proposed 40% mining tax; this may have been a primer, but dissatisfaction runs deeper. As fears of Australia's vulnerability to falling Asian import markets (Australian raw material), goverment deficits, inflation and over leveraged housing may also been a unsettling dilemma for Australian voters. The point being is although the new prime minister Julia Gillard has now allowed miners a free ride by attaching the mining tax to the 10yr Aussie bond (it falls, so does the tax threshold). The big questions is when Australian begins to slow down, and this should be a rapid decent into the last 6mths of 2010. Will the new prime minster and her party initiate a 2nd round of stimulus? Since the budget deficit for Australia is 56+billion (for a population 21million - a tax receipt short fall from hell) if she does and sends the Australian deficit further into the red, no doubt the Aussie bond yields will go upward and bond vigilantes will start to look at Australia and price in higher yield offerings; thus effecting Australia's credit rating (such as the European PIIGS)

What is left is the high yielding Australian dollar, whilst we have deprecating currencies global, the AUD has been bought for it's high yield and desirability for Japanese carry traders. In 2008 I successful held a put on the AUD refer to AUD put 2010. It was my "go for the jugular" George Soros moment, admittedly the return was (very) micro compared to his "1billion dollars" in one day betting against the GBP ( UK pound) in 1992. Still in 2010 we have have a another 'jugular moment' brewing for the AUD as the Reserve Bank of Australia will start to cut rates in the next 6mths.

refer to chart AUD/USD:

the support (breach) is 0.80

a swing point (monthly chart) down at 0.87.

{kind=link}

Subscribe to:

Comments (Atom)